Since we began publishing our digital challenger bank list, Novo has been the most popular choice (though recently, Mercury has surpassed it). Today, I thought I’d drop by Novo’s website and see what’s fueling its success (see also, our previous post, Sep 2021).

The first thing you notice is the clear focus on small business banking. Unlike large commercial banks, where it takes a bit of poking around to find small business products, Novo is all business. They have just four main nav items:

- Business checking

- Our customers

- About us

- Help

Most prospective customers will hit the “Business checking” button and immediately see a list of core features:

- Features

- Novo Apps

- Novo Boost

- Reserves

- Invoices

- Perks

You might notice a major, major item missing from these 10 core areas, PRICING. It’s one thing if Wells Fargo leaves that off, that’s expected. But a modern digital player is expected to be very transparent with pricing. Novo doesn’t even address it in their FAQs, if you search for “Pricing” it merely shows two links to info about partner prices (Quickbooks and Wise). Novo is seemingly a breakout success with 175,000 customers and 1.2M visitors per month (tied with Mercury for #1 in traffic) but if they addressed pricing more directly they might have 300,000 customers!

Back to its differentiating features. There are two important areas:

- Boost: This is a service that posts revenue quicker than the typical 1-3 days from traditional players. Details are sketchy, but Novo likely uses the integrations to Stripe, Wise, etc to post funds ahead of scheduled ACH transfers. Again, the feature would be much more of a competitive advantage if Novo did a better job explaining how it works.

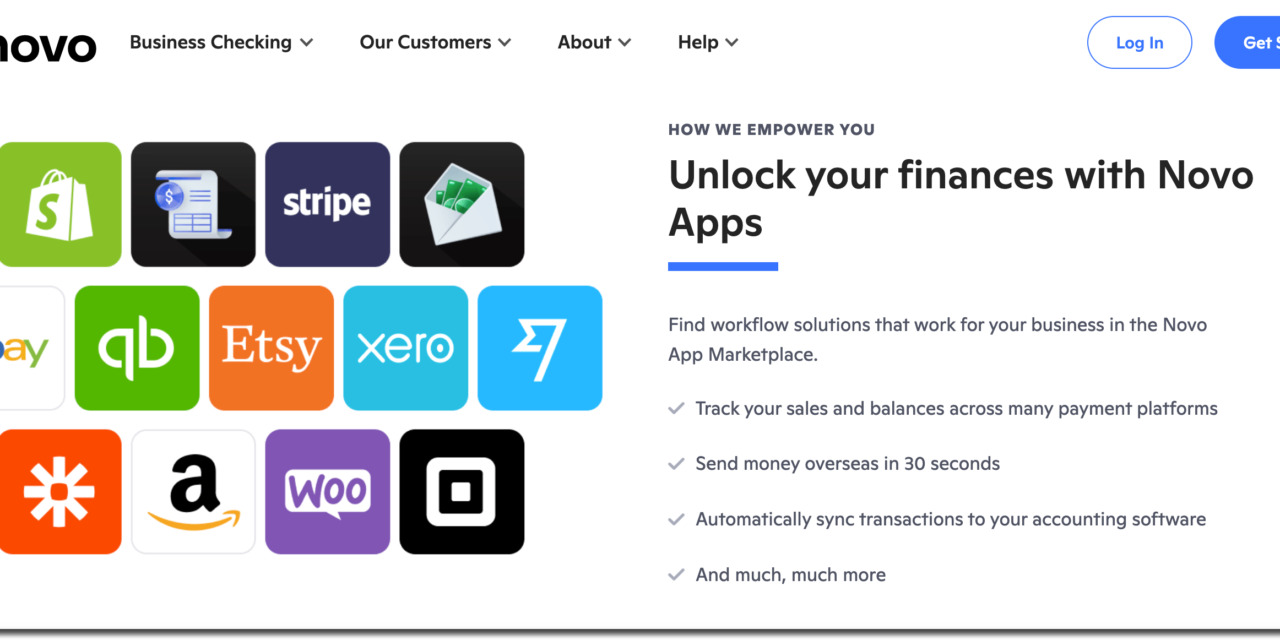

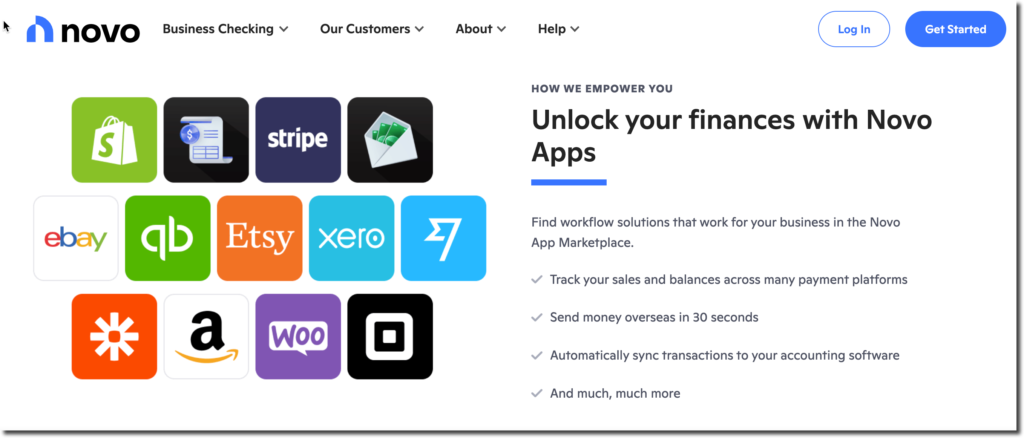

- Novo Apps: One of the most powerful features of modern online banking services is their ability to integrate with other ecommerce sites through the bank-run dashboard. Nova advertises integrations with 13 services (see top screenshot), but per usual, does almost nothing to explain how they work, the benefits of the apps, or even what the term means.

The other two listed items are not as important in terms of differentiating Novo from its peers:

- Invoices: This is the most straightforward of the feature set. The ability to send invoices with integrated credit card and electronic payment options. It’s an important feature, but not really a differentiating factor as it’s pretty much table stakes for digital small business banks.

- Reserves: I don’t love this name, since it makes me think of a credit line. In fact, it’s the opposite. A feature that allows customers to easily set up dedicated savings accounts for various purposes. It’s not nearly as important as the first two items, but since it’s much easier to understand, it makes sense that it would be featured on the website.

Company vitals

Novo

FAB Score: 297 (#2 after Mercury)

– HQ: NYC

– Founded: 2016

– Raised $136M including $131M in 2021 (Crunchbase) <<< Most raised since Jan 2021

– App downloads (last 30 days): 56,000 (Apptopia)

– Website visits: 1.2 mil (June 2022; SimilarWeb) <<< Highest in category (tied with Mercury)

– Employees: 269 (Pitchbook)

– Articles: 90 (Crunchbase)

– Linkedin: 12,300 followers (270 employees)

– Twitter: 2,200 followers

– Industry awards: 4 (Novo)

– Integrations: Wise, Xero, Slack

– TrustPilot: 3.4 (1,160 reviews)

– iOS app: 4.8 (11,100 reviews) <<< Tied for highest score with several others

Note: Fintechlabs earns referral fees from several financial services providers. At the time of publication, both Novo and Mercury compensate us for new accounts.

{kind=link}