Fine-tune the User Experience (UX) With Authorizing New Card Users

As financial institutions digitize every product, process and procedure, there are thousands of tweaks necessary to fine-tune the user experience. For example (from our mobile UX framework):

#132. Is it intuitive how add a new authorized credit or debit card users?

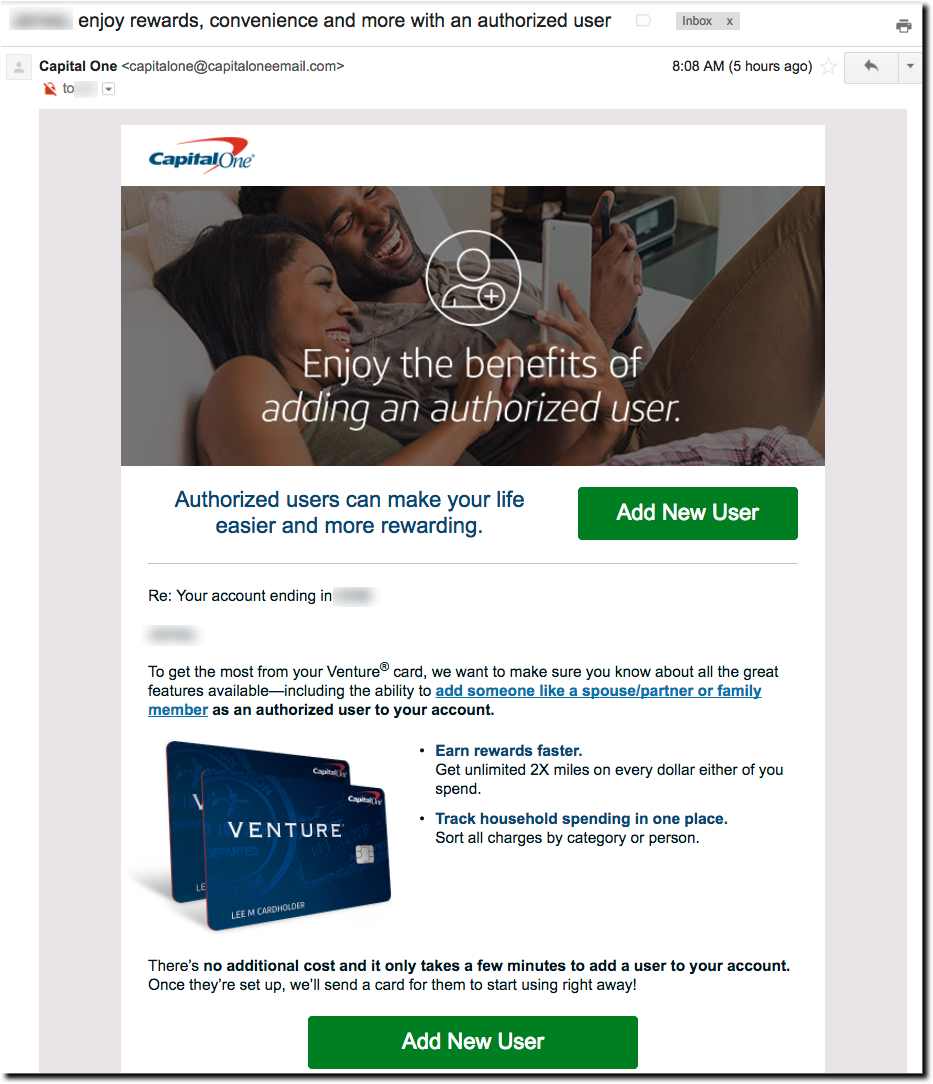

We’ll use Capital One to illustrate the finer points since just yesterday I received their email with that suggestion (see screenshot above).

We love the business case here. Adding an authorized user is a win-win. The card issuer boosts spend by adding another cardholder. And it helps the original cardholder better manage household (or business) spending with multiple users rolled into a single account. The Capital One email message did its job catching our attention.

But once we dove into the actual process, it was a little less than ideal. No major issues, but a half-dozen things to improve.

The Process

The email is straightforward and well done. Just press either of the green buttons to get started. However, there is one major disconnect here. How do you know it’s a legit email? Granted, Capital One followed best practices with first-name personalization and the last 4 digits of the card number. But, the bank doesn’t directly address security concerns. So it’s message is ignored by a significant chunk of customers who have rightfully grown suspicious of financial emails.

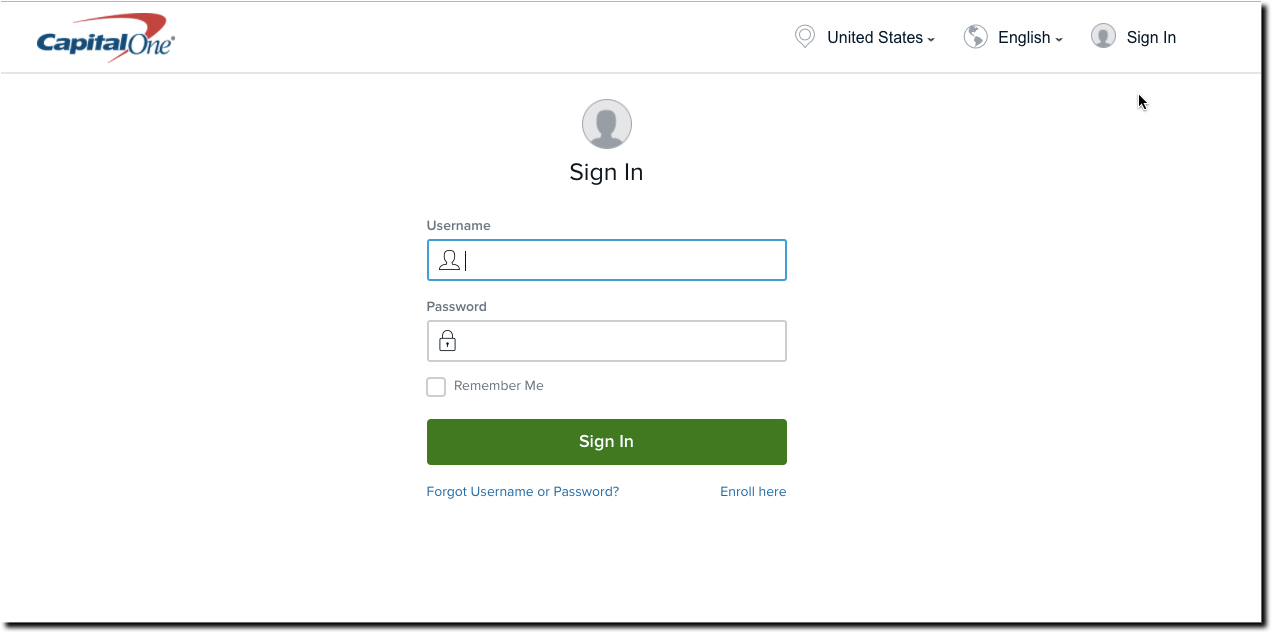

Customers willing to go further click on the green button and are transported to a blank login page (see #1 below). This is where Capital One bungles the process in several ways.

- No security reassurances: A blank page is not what I expected when I clicked through the email. There should be a nicely designed landing page with FAQs addressing security concerns along with instructions on how to add a user by going to Capital One directly and logging in.

- No marketing reinforcement: You are trying to sell a customer on adding a new user, which could add hundreds of dollars to your bottom line. Let’s help them go deeper into the sales funnel by encouraging them to log in and complete the process.

- Not focused on the matter at hand: Even if customers are trusting enough to log in, the bank still throws a random cross-sales message at them first (see screenshot #2 below). Capital One wondered if I might want to save money on a balance transfer. It’s a good offer with a 3% charge and no interested for 18 months, but it has nothing to do with adding another user.

Once the user swats that banner away, the process is pretty straightforward.

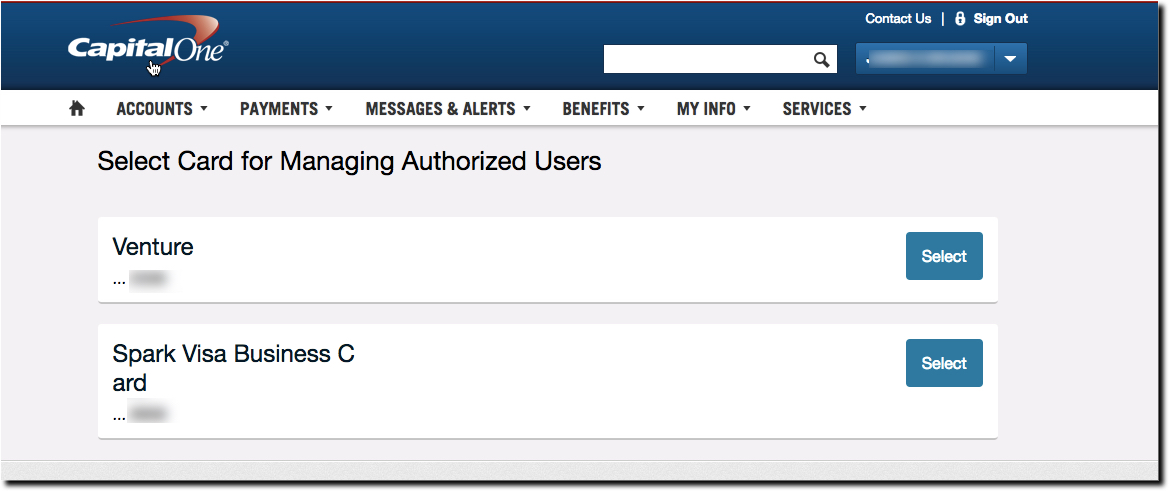

- Choose which credit card account (screenshot #3)

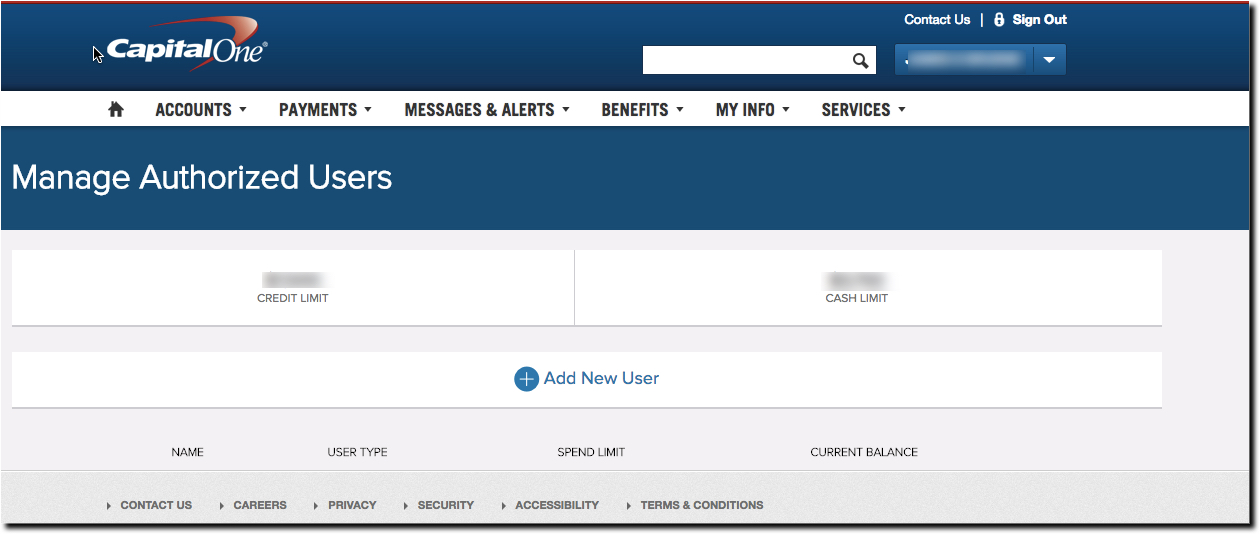

- In manage cardholders, select “Add New User (screenshot #4)

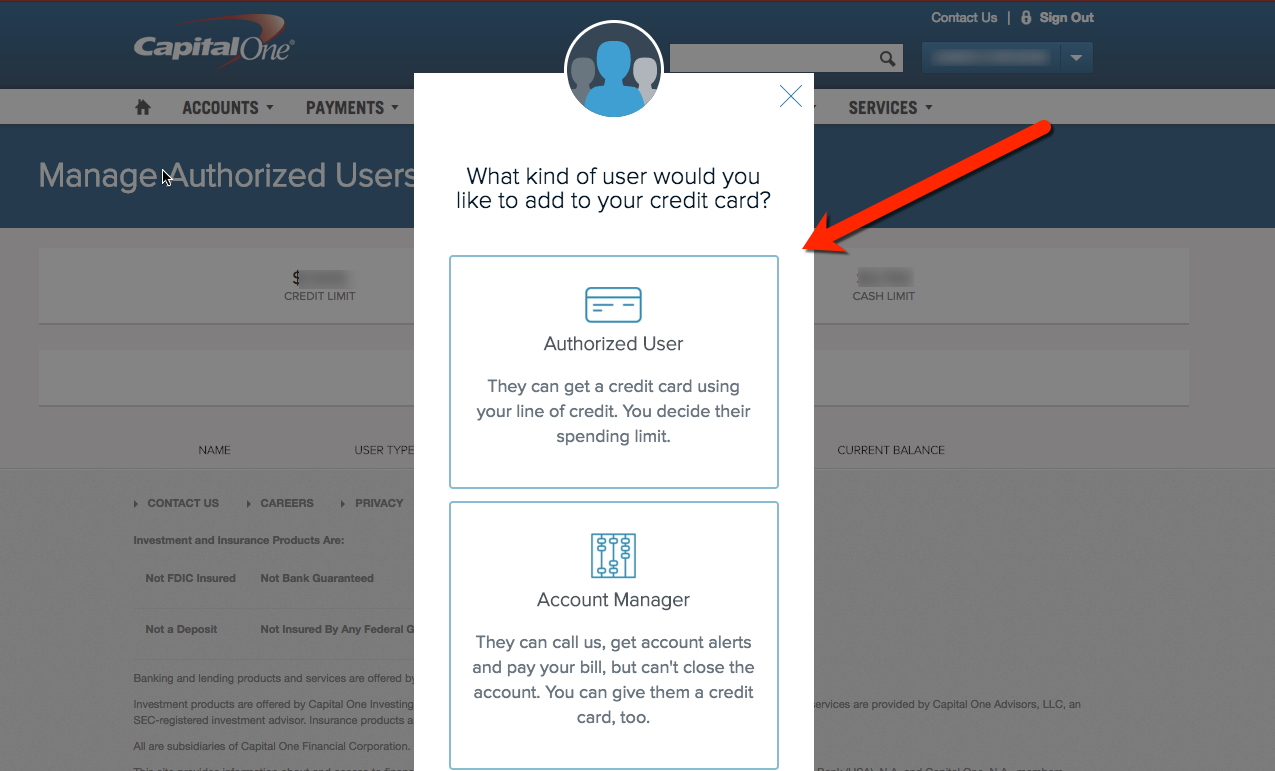

- Select what level of permissions for the new user (screenshot #5)

- Provide contact info for the new user (screenshot #6)

Our main complaint here is that there is no FAQ or links for help. Customers will wonder: Why do you need the social security number? Will there be a credit inquiry on the new user? How much does it cost? What if there are unauthorized charges? What happens next? And so on.

Bottom line: Customers have many questions and concerns about credit issues, so you should address the major ones during the process of authorizing a new card user.

And it’s also worth providing customer support options at this point, especially online chat to address these major questions.

Screenshot 1: Login after clicking through email

Screenshot 2: Select card

Screenshot 3: Manage cardholder, add user

Screenshot 4: Select permissions

Screenshot 5: Fill out info on new cardholder

{kind=link}