Financial institutions play a long game. Unlike most startups which measure the long-term value of new customers in years or even months, in the digital age, there is no reason why banks can’t hold onto customers for multiple generations. If they’d had online banking, I’d probably still be a loyal customer of National Bank of Gladbrook.

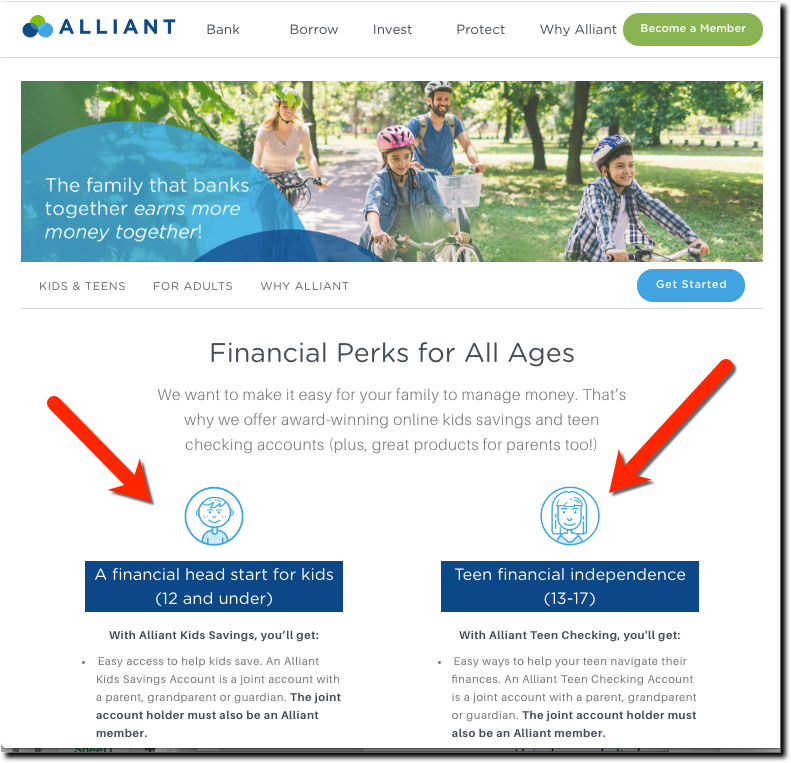

But to retain your customers, and importantly their children, you need to create digital services that keep the family together, financially anyway. See above for Alliant Credit Union’s youth account lineup. Here’s a rough roadmap for supporting the five stages of growing up financially:

- At birth: Offer identity protection and credit monitoring to avoid early-age fraud (see WSJ today on that growing threat)

- Age 5 to 10: Savings account so parents and grandparents can help junior start the savings habit early.

- Age 11 to 13: Add a debit card (ideally with parental controls)

- Age 14 to 15: Add simple budgeting & spending tools

- Age 16 to 17: Add services centering on college, rental matters, and early work life.

Most importantly, every child’s account should be tied closely to the parents for instant funds transfer through easy-to-use mobile, online and voice interfaces.

{kind=link}