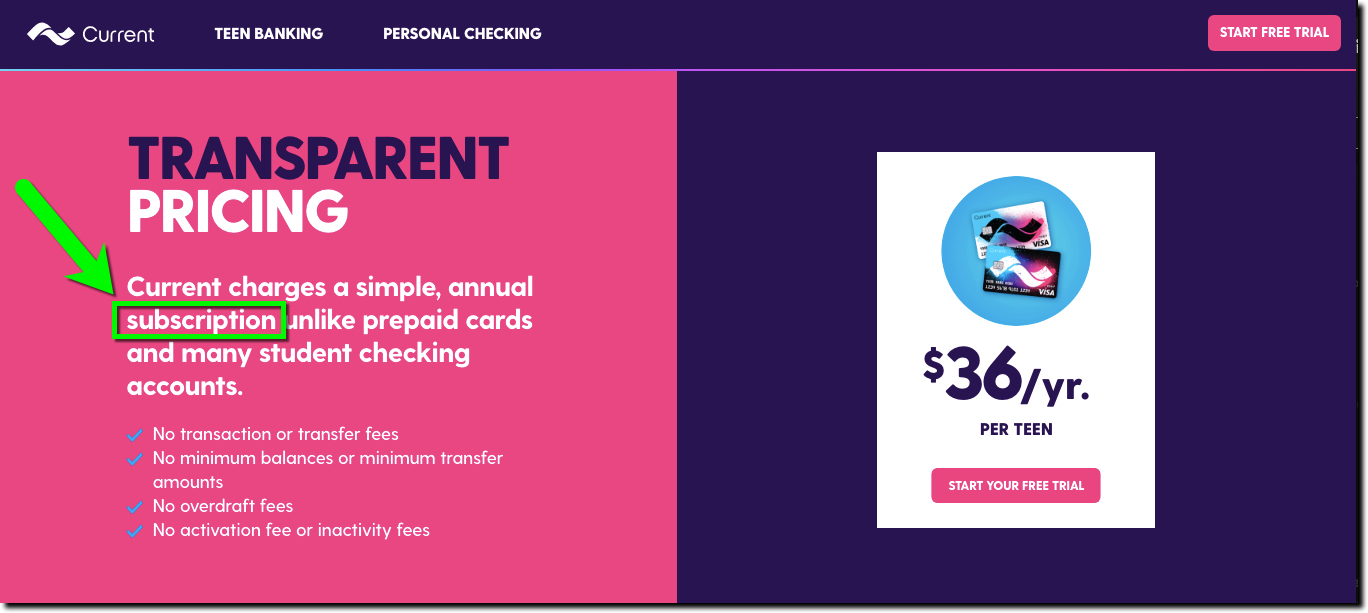

Current card emphasizes its transparent annual subscription

Most consumer banking research finds that “high fees” are one of three or four primary reasons to close an account. But what does that mean? Is it transaction fees at the ATM? Monthly checking account fees? Or penalty fees from overdrafting? I suspect it's often the latter, but you can lose customers over anything you charge them. And it drives bankers crazy realizing that tens of millions of customers will stand in line for a $4 cup of coffee but $4 or $5 a MONTH for a checking account sends customers packing.

But consumers don't view bank fees the same way they look at other consumer purchases. Here are common myths which leave customers wondering if they are being taken advantage of:

- The bank gets to use MY money: Most consumers vastly over-estimate how much value banks derive from the money in their checking account, especially in relatively low-rate periods.

- I'm a great customer, never causing problems: Most consumers vastly under-estimate how much it costs to provide secure banking services in a highly regulated market, not to mention responsive customer service.

- Every bank is the same: Most consumers don't really have a bond with their bank (though credit unions are often a different story), but they view it as too much of a hassle to move to what they perceive as similar service elsewhere.

How do you fight these perceptions?

- Minimize penalty fees (especially for overdrafts) and introduce subscriptions

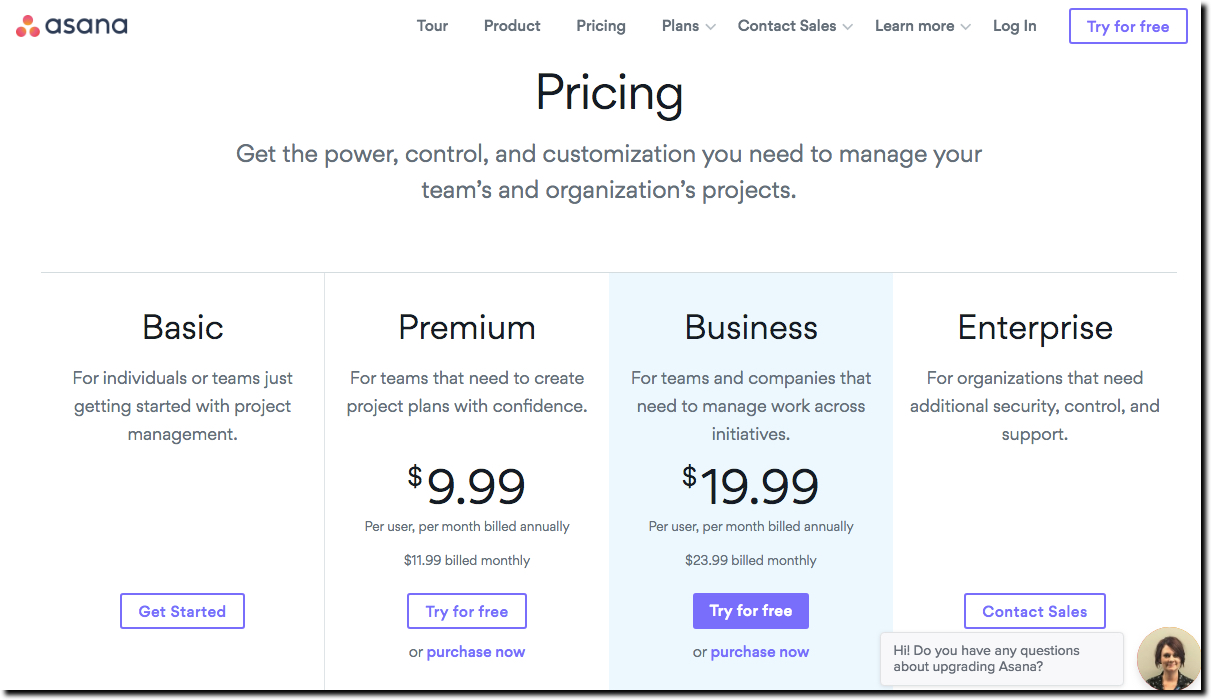

Behave like a tech company (see Asana pricing screenshot below) and introduce monthly or annual SUBSCRIPTION for a bundle of digital services. This will go a long way in differentiating you from your neighbors. - Create a variety of premium subscription types

Because banks offer services to a wide variety of customers, prices shouldn't be one-size-fits-all. Look at SaaS companies with basic services for free and with varying monthly fee packages for PREMIUM or PRO level benefits. - Add gamification to every subscription level:

Why does my electric utility do more with game mechanics than my bank? For decades, utilities show the amount used this month compared to previous months and most importantly the year earlier. This is vital feedback for customers who care about saving money (or the planet). Banks should be doing the same same thing showing savings, spending, interest earned, customer services calls, bills paid, etc over time.

{kind=link}